You've opened a 529 plan and started saving for a friend or loved one's education. The hard part—actually setting the money aside—is done.

Now comes the next question: How do you invest it?

To answer that, we need to survey the landscape. What does Vanguard actually offer in your particular 529 plan—and how do those options differ across plans?

It’s worth setting expectations up front. For many investors, the Target Enrollment series will be the easiest choice—fast, sensible and simple. But it’s not the only option, and understanding what’s under the hood will help you decide whether or not to go your own way.

If you're still deciding whether a 529 plan is right for you, start here—I covered the basics last week.

Key Points

- Vanguard's 529 plans vary more than you'd expect.

- Within any plan, you can build your own portfolio from individual funds or hand the wheel to Vanguard.

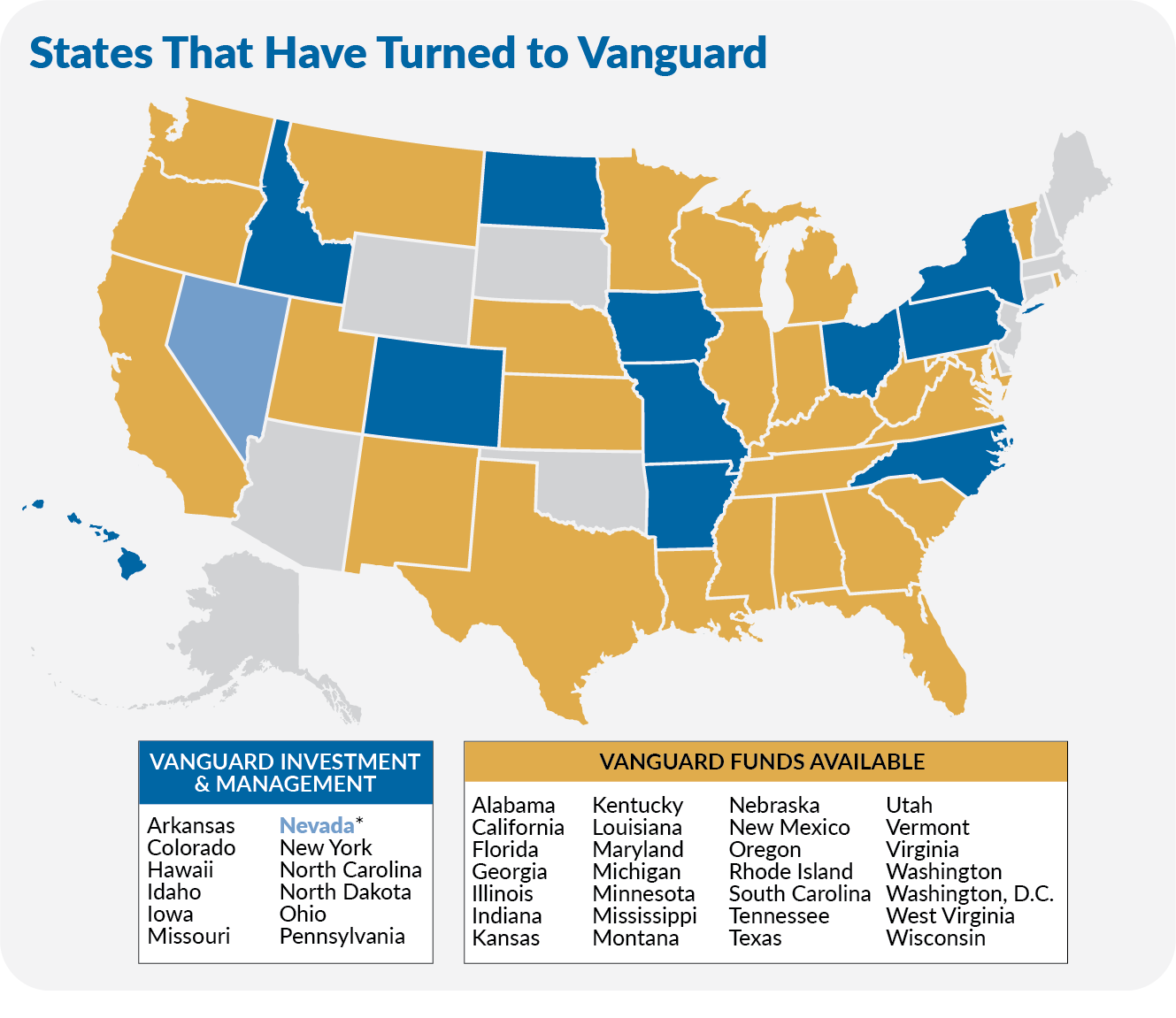

Vanguard’s 529 Footprint

As I noted last week, every state except Wyoming offers its own 529 plan, sponsored by one or more investment managers. Vanguard funds are available in 38 states plus Washington, D.C.

Vanguard is more deeply "associated" with plans from 12 states—meaning it has been hired as the program manager or serves as the plan's investment manager. Only one of those plans, Nevada's, is marketed and sold as "The Vanguard 529 Plan." More on that in a moment.

It's hard to generalize across these plans because each one is different. A 529 plan isn’t just “a Vanguard plan”—it’s a specific state plan with its own menu, structure and quirks. That matters more than most investors realize.

Also, Vanguard changes its thinking on the right way to invest for college from time to time—and when it does, it can take years for those changes to reach all the plans it manages, if it does at all.

Case in point: Vanguard introduced its Target Enrollment series—think Target Retirement funds for college—in Nevada's plan back in 2020. Six years later, four plans are still using older age-based tracks.

That said, Vanguard-associated plans typically offer a mix of single-fund choices and multi-fund portfolios. Some multi-fund portfolios are static; others shift automatically as the beneficiary ages. And across the board, Vanguard takes an index-heavy approach—four total market index funds are the primary building blocks.

The table below summarizes the 12 plans where Vanguard both manages and provides the investments for 529 savers.

Plans "Associated" With Vanguard

| State | # of Individual & Multi-Fund Portfolios | # of Age-Based Tracks | Age-Based Track Increments | Target Enrollment Track? | Expenses |

| Arkansas | 7 | 0 | N/A | Yes | 0.39%–0.53% |

| Colorado | 10 | 3 | 12.5% | No | 0.27% |

| Hawaii | 8 | 1 | 12.5% | No | 0.58%–0.66% |

| Idaho | 7 | 0 | N/A | Yes | 0.34%–0.36% |

| Iowa | 14 | 0 | N/A | Yes | 0.17% |

| Missouri | 17 | 3 | 10.0% | No | 0.16%–0.41% |

| Nevada | 25 | 0 | N/A | Yes | 0.11%–0.49% |

| New York | 18 | 0 | N/A | Yes | 0.11% |

| North Carolina | 10 | 3 | 12.5% | No | 0.25%–0.36% |

| North Dakota | 6 | 0 | N/A | Yes | 0.48%–0.83% |

| Ohio | 20 | 0 | N/A | Yes | 0.00%–0.44% |

| Pennsylvania | 14 | 0 | N/A | Yes | 0.18%–0.27% |

The simplest plans—Arkansas, Idaho and North Dakota—offer just the Target Enrollment series, a handful of multi-fund portfolios and a cash option. Hawaii is similarly streamlined, though it still uses age-based tracks.

At the other end of the spectrum, Nevada’s plan offers the Target Enrollment series, six static multi-fund portfolios and 18 individual fund choices.

Hold the China

Digging through the Plan Disclosure documents, I noticed that two plans—Arkansas and Missouri—quietly started using Emerging Markets ex-China ETF (EMXC) in late 2025.

Missouri took the opt-in approach: it added an International Stock ex-China Portfolio—an 80/20 mix of Developed Markets Index (VTMGX) and Emerging Markets ex-China ETF—as a standalone option alongside the standard Total International Stock Index Portfolio, giving investors a choice of including Chinese stocks in their portfolios or not.

Arkansas went further. It replaced Total International Stock Index with that same 80/20 ex-China mix across all Target Enrollment and static multi-fund portfolios—meaning no participant in the Arkansas plan owns Chinese stocks, whether they know it or not.

China, for better or worse, accounts for 8% of the non-U.S. market capitalization—only three countries are larger. Excluding it is a big call to make on behalf of investors.

Whether you agree or not, it’s a reminder that in a 529 plan, you don’t always control the underlying portfolio decisions.

Each plan is different, and you'll want to confirm what's available in your state. Now let's take a closer look at The Vanguard 529 Plan.

The Vanguard 529 Plan

The name isn't an accident. Nevada's plan is the one Vanguard brands, markets and actively develops as its flagship. Try to open a 529 account on Vanguard's website, and it's your only option.

If your home state doesn't offer a tax break—or if its plan simply doesn't measure up—this is a natural alternative. It offers the broadest fund lineup and is open to investors in any state. But feel free to shop around, and know that "Vanguard" in the name doesn't automatically mean lowest cost; New York’s plan, for example, is cheaper.

Like nearly all 529 plans, The Vanguard 529 Plan gives college savers two main choices: