What if you could lock in a tax break for charitable giving today—and decide who gets the money years from now?

That’s the appeal of Vanguard’s Charitable Endowment Program (VCEP). It’s a simple, low-cost way to separate the timing of your tax deduction from the timing of your giving—and for many investors, it’s about as close as you can get to running your own charitable foundation without the hassle.

How It Works

Vanguard’s program, like similar ones at Fidelity, Charles Schwab and other financial institutions, is known as a donor-advised fund (or DAF).

You can donate various assets to the program, including stocks, bonds, cash, fund shares and other marketable securities. The assets will be sold, with the proceeds going into one (or more) of the 36 investment portfolios (called “pools”) of your choosing. These assets become part of your personal charitable account, titled (nearly) any way you like.

The beauty of the Vanguard program is that it allows you to donate your assets to the Endowment and take the tax deduction now. Plus, if you contribute securities that have appreciated, you avoid paying taxes on those gains.

Then, you have years to decide where the money should go. When you make donations from your charitable account, you can do so anonymously or with recognition.

As for the program's logistics, it’s pretty simple. Technically, once you donate assets, you no longer control them. However, in practice, this is, as the name implies, a donor-advised fund. Vanguard Charitable follows your recommendations on how to invest and where to give. If it didn’t, the program wouldn’t work—and it wouldn’t attract billions in annual donations.

Giving a Lot

And attract money it has!

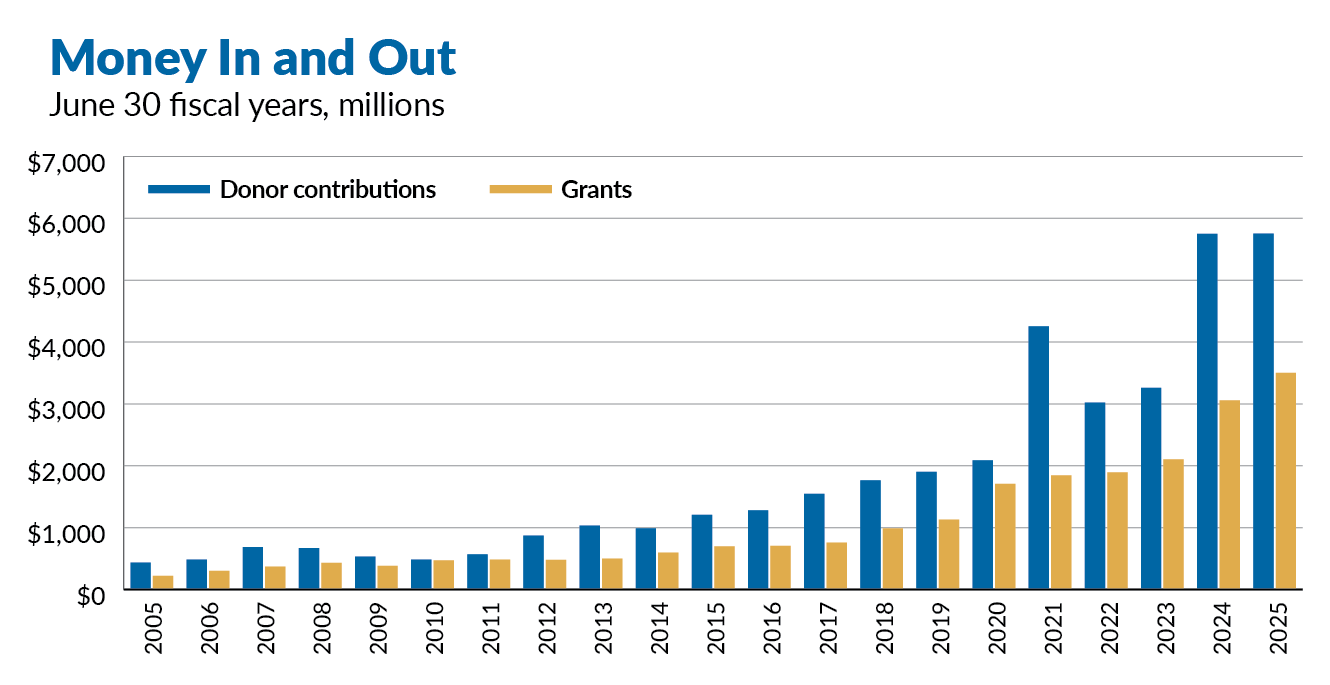

Since registering with the Internal Revenue Service in December 1997, VCEP has grown dramatically. Donors have contributed more than $5 billion in each of the last two years. In the fiscal year ending in June 2025, VCEP held nearly $26 billion—up from about $15 billion at the end of June 2022.

In each of the past two fiscal years, program grants topped $3 billion.

In other words, this isn’t a niche program—it’s become one of the largest donor-advised funds in the country.

If you’re looking for a near-equivalent of your own charitable foundation without the hassles and the tax filing requirements, here’s what else you need to know.

Getting Started

To start, you need to give the program at least $25,000. (Subsequent gifts must be $5,000 or more.) You can also get a group of family, friends or associates together and each donate $5,000 (totaling $25,000 or more) to open a joint account.

Your account will fall into one of two tiers: Standard or Premier.

Premier status is typically for those with balances greater than $1 million for at least three months—though VCEP says it is subject to approval. It features reduced administrative fees and the additional benefit of a dedicated service team, which Vanguard calls its Premier Services.

When opening your account, you’ll need to give it a name. As long as it starts with “The,” ends with “Fund,” and doesn’t include “trust,” “foundation,” or “endowment,” you can name it as you want. For instance, I could name mine The Jeff D Fund if the name wasn’t already taken.

However, keep in mind that the name will appear in communication and grants (unless you give anonymously). Also, Vanguard Charitable reserves the right to deny account names.

When you’re getting started, counterintuitively, is also when you need to think about the end of the plan—or at least the end of your time with it. You’ll want to set up (or recommend) a succession plan for Vanguard Charitable to follow after your passing.

You have a few options to choose from—you can pick one option or mix and match:

- Pass the account on to another, like a spouse or child, who will assume “control”

- Create new accounts—useful if you wanted to, say, split the account for two children

- Recommend a final lump-sum grant

- Make recurring grants through an “Endowment Grant Program”

- Transfer the account to Vanguard Charitable’s Philanthropic Impact Fund or Sustainable Disaster-Relief Fund, which is run by a board of Vanguard trustees that makes all grant decisions

You don’t have to create a succession plan, but if you don’t, any money left in the account will go to the Sustainable Disaster-Relief Fund or Philanthropic Impact Fund.

Giving to Keep Control

Once your account is set up, the next question is how you manage it over time.