Executive Summary: Should you be a growth investor or a value investor? After three decades of Vanguard returns, the answer appears to be neither. Growth wins in some markets, value wins in others, and even the academics who popularized the so-called “value premium” later admitted the evidence was too noisy to settle the question.

Is it better to be an investor who focuses on growth stocks or one who goes the value route? Based on recent history, the answer seems obvious: growth, by a mile. But spend any time with the academic literature, and you’ll hear the opposite—that value stocks are destined to win over the long run.

So, which is it?

My bottom line on the growth versus value debate is that neither can be reasonably assured of winning all the time or even over time. Each style will have its days in the sun and days in the doghouse. The right move isn’t picking a side—it’s eschewing the labels while holding a well-diversified portfolio.

Now, let me make the case for that view as the market’s growth stocks scale new heights and the value camp says, “Just you wait.”

Investing in the Real World

While the growth versus value question has been studied endlessly, Nobel Prize winner Eugene Fama and his colleague Ken French put the “value premium” (the idea that value stocks outperform growth stocks) on the map with their 1992 article The Cross-Section of Expected Stock Returns. (Fair warning: It’s a dense academic paper.)

Conveniently, just five months after Fama and French published their academic findings, Vanguard launched two index funds, Growth Index (VIGAX) and Value Index (VVIAX), and inadvertently gave the warring sides an opportunity to test the academics in the real world.

So, have Vanguard investors with a value bias matched the academics’ expectations? (Spoiler alert: No!)

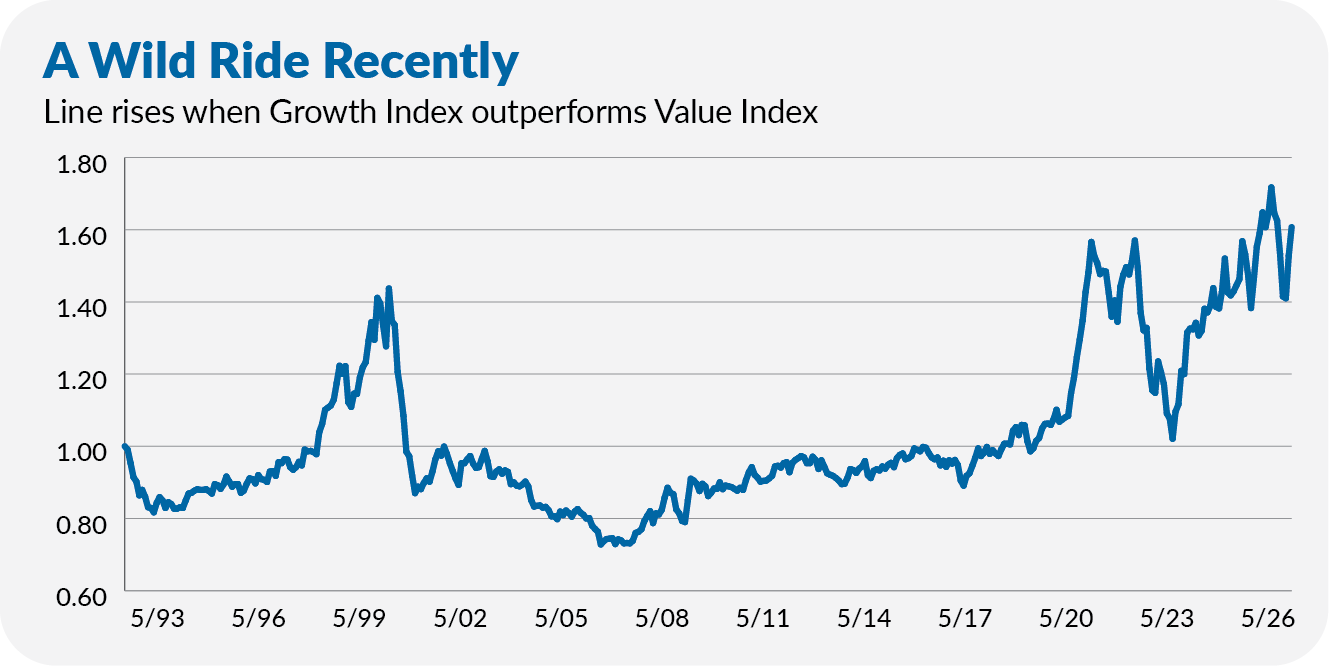

The chart below compares Growth Index and Value Index since their 1992 inception—almost 35 years ago. The line rises when growth leads and falls when value leads.

At inception, Value Index briefly outperformed out of the gate (the line falls), but for most of the 1990s, Growth Index carried the day (the line rises). Value stocks recouped their underperformance very quickly as the tech bubble burst (the line fell sharply in 2000), and they continued to lead until the Global Financial Crisis upended markets between 2007 and 2009.

Growth stocks outperformed in the 2010s (the line rises), and by the end of 2019, growth and value stocks were pretty much even.

Things changed in 2020, and we’ve seen some dramatic swings in the relative fortunes of growth and value stocks since then. Growth stocks thrived during the pandemic and its immediate aftermath, but they tumbled when inflation and interest rates rose in 2022.

Beginning in 2023, though, an artificial-intelligence-fueled rally has seen growth stocks race ahead of their value siblings. Growth stocks are now leading value stocks by more than during either the tech bubble or the post-pandemic rebound.

So, yes, after more than 33 years, Growth Index is ahead of Value Index, 3,965% to 2,429%. That’s 11.7% per year for the growth fund and 10.1% for the value fund.

Three thousand dollars (the funds’ minimums at inception) invested in each of the growth and value index options would have grown to nearly $121,960 and $75,881. That 1.6% annualized difference in returns has compounded mightily for growth adherents.

But this single point-in-time return doesn’t convince me that being a growth investor is better. If there is anything to take away from the numbers I just cited, it's that both value and growth investors compounded their money at attractive rates.

An important takeaway from the chart that I think many investors might miss is that being either a growth or a value investor is hard! Since 1992, investors who focused on either of the two styles have felt like geniuses and buffoons.

If in 1992 you’d ignored Vanguard’s shiny new growth and value index funds in favor of the tried-and-true 500 Index (VFIAX), you compounded at an 11.0% rate for the past nearly 35 years. Your $3,000 would be worth $98,410—not as much as a growth investor’s portfolio, but better than the value investor’s result.

The truth is that owning both growth and value stocks is a lot better and easier on your psyche than owning one and ignoring the other.

It Depends Where You Look

The AI era has added a new wrinkle.