Six months ago, when Vanguard announced it was handing MidCap Growth (VMGRX) over to Tremblant Capital, I welcomed the shift—from a sleepy, index-hugging portfolio to what I hoped would become a truly active, aggressive mid-cap growth fund. That said, I also cautioned against rushing in.

Taxes were one reason to be patient. The other was simpler: Tremblant is a new name for most Vanguard investors. And before partnering with any active manager, I want to do the homework and build conviction.

In February, I started that process by popping the hood on the fund’s new portfolio. And, as I told you the other week, I have small “trial” (or “research”) positions in MidCap Growth and Tremblant Global ETF. Today, I’m taking the next step—sharing my conversation with Tremblant’s co-CIOs, Brett Barakett and Michael Cling.

We spoke on March 4. I’ve kept the editing light and the transcript long so you can hear directly from the managers and draw your own conclusions. But before we get there, here are my key takeaways:

First, this is now an aggressive fund.

MidCap Growth will typically hold 45 to 60 stocks. It’s not built around a handful of high-conviction bets—instead, Barakett aims to win through a high hit rate across a diversified set of ideas.

That doesn’t mean it’s defensive—quite the opposite. Tremblant’s portfolios tend to get hit when volatility spikes. But historically, they’ve used those periods to their advantage—and have come out stronger on the other side.

Second, they’re betting on “consequential change” … with some guardrails.

Tremblant’s edge, in their view, comes from identifying companies undergoing meaningful change—situations where the market is misjudging what a business will look like a year or two down the road.

They do this through deep, fundamental research, aiming to understand businesses at a level beyond management’s own narrative—focusing on the key drivers that separate signal from noise.

Importantly, this isn’t a freewheeling, go-anywhere portfolio. The fund is still managed with an eye on its benchmark. Think of it as a mid-cap growth portfolio with targeted bets on companies undergoing material change—not a pure expression of Tremblant’s highest-conviction ideas.

(If you want that, they offer it in ETF form via Tremblant Global ETF (TOGA), without the same guardrails.)

Why Tremblant?

When I asked Vanguard (in a follow-up conversation) why it chose Tremblant, a firm that has never run a dedicated mid-sized stock strategy, the answer was telling: The manager search team was encouraged to “think creatively.”

Vanguard had been watching and speaking with Tremblant for years. And when they dug into the firm’s track record, they found that many of its best ideas—and much of its outperformance—came from mid-sized companies.

They decided to collaborate, betting that Tremblant could apply its approach within the structure of a mid-cap growth fund.

Time will tell whether that out-of-the-box thinking pays off.

What Performance Tells Us (So Far)

It’s still early—just a few months of data—so I wouldn’t read too much into it. But we can begin to see whether the results line up with expectations.

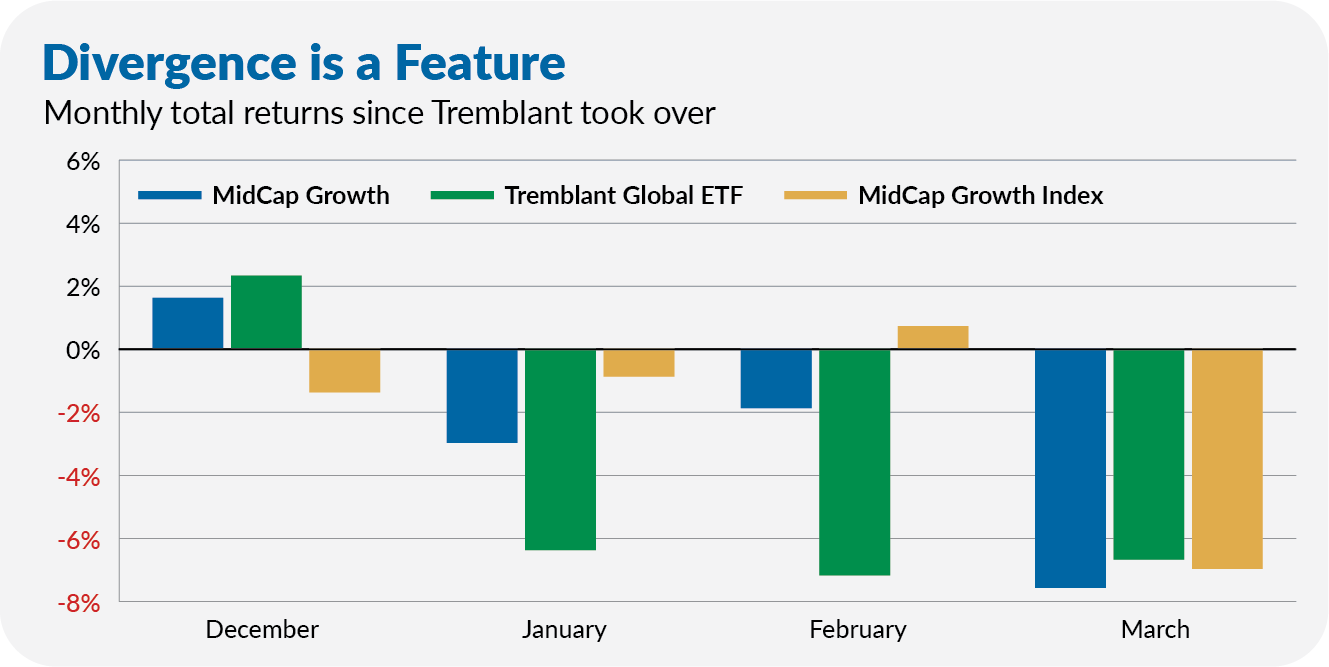

Since Tremblant took over MidCap Growth’s portfolio, from Nov. 14, 2025, through Mar. 20, 2026, the active fund has trailed MidCap Growth Index -10.9% to -7.8%.

Looking at the funds’ monthly returns helps tell the story. In the chart below, I’ve also included Tremblant’s TOGA ETF.

Tremblant got off to a strong start—both MidCap Growth and TOGA outperformed in December. But that momentum didn’t last. Tremblant’s stock picks faltered in January and February as concerns around artificial intelligence (AI) disruption sent traders scrambling.

You can see this most clearly in TOGA, which fell 6.4% and 7.2% in the first two months of the year. MidCap Growth was down as well, but the better risk controls it has in place did their job.

So far in March, all three funds have declined by similar amounts as the Iran war has led to broad-based selling.

It’s early days, but the initial results line up with what you’d expect:

- Returns have been broadly in line with the index.

- MidCap Growth has fallen harder during bouts of volatility.

- Performance is being driven by stock selection—both positively and negatively.

- Compared to Tremblant’s ETF, the mutual fund shows tighter risk controls.

In short: MidCap Growth is a more active, more volatile—and more differentiated—fund with Tremblant stirring the pot than it was with multiple sub-advisors in the kitchen.

What we don’t have yet is an important test: How the fund performs when markets rebound.

I’m watching closely.

Without further ado, here is my conversation with Tremblant Capital’s Brett Barakett and Michael Cling:

Before I look at performance, I want to understand the people, the process, the philosophy and the portfolio. So, let’s focus on that today as we get to know Tremblant Capital. Please start at the beginning with an intro to the firm, Brett, Mike and the team.

Brett Barakett (BB): Roughly 25 years ago this month, I started on the journey of starting Tremblant Capital—originally as a long-short hedge fund. Back in 2001, hedge funds were on the ascendancy.

In 2011, we launched a long-only strategy. Since then, we've done multiple things to meet the needs of different clients. Prior to becoming the sub-advisor for Vanguard, we launched our own ETF (ticker TOGA).

Along the way, Vanguard started a string of conversations with us about how we might be helpful—and ultimately selected us to manage the MidCap Growth fund for them.

As for my personal background, I'm a Canadian from Montreal.

I went to the Ivey Business School in Ontario. Neither of my parents graduated from high school, so I didn’t have much guidance. I just knew I liked business and that Ivey was considered the top one in Canada. So, I went there for undergrad.

Out of school, I got a job at Procter & Gamble. Again, I had no clue, but one of the professors at Ivey said, “They're one of the best-run companies in the world. They primarily promote from within. So they'll develop you. They're incentivized to develop you, and give you a business to run and call you a brand manager.” So, I did that.

Then one of my brothers had drifted down to the US to play ice hockey. He then decided to go to Harvard Business School. He convinced me that I should go as well, and we ended up going the same year.

After that, I joined Reebok—again because I like operating businesses. I saw my peers go to Wall Street—specifically, hedge funds—in the early to mid-90s, which intrigued me. After some research, I followed.

I was on the sell side briefly before working at another hedge fund. And then, as I said, in 2001, we launched Tremblant.

The most important part of my background is that my first career was as an operating manager, followed by a financial manager role. That is a differentiating factor: being able to think through how a business operates and then applying financial analysis on top of that.

Michael Cling (MC): I joined Tremblant in March of 2005 as an analyst covering the technology, media and telecom sector. I became the team lead in 2009 and, ultimately, a partner at the firm in 2012. I’ve really had a series of ever-expanding roles since 2012, culminating in being the co-CIO with Brett on this product for Vanguard.

Prior to Tremblant, from 2002 to 2005, I worked at a hedge fund called Ivory Capital in Los Angeles. That was really my introduction and education in investing in public markets.

Ivory Capital’s investment style was what I would call a deep value strategy. If you go back to the old days of hedge funds, that style was in vogue—that alpha-harvesting opportunity in public markets then was certainly much more conducive to that style.

Before that, I worked at Blackstone's Private Equity Group, which gave me a foundation for evaluating businesses. It taught me the importance of structuring a balance sheet properly and the appropriate use of leverage to enhance returns on invested capital. Of course, I also saw situations where excessive leverage destroyed quite a bit of capital.

Before that, I spent a couple of years as an investment banking analyst at Lehman Brothers, which was my first job out of college. I attended Georgetown University and graduated in 1998.

Michael, what attracted you to Tremblant?

MC: I noticed during my time at Ivory Capital—between 2002 and 2005—that the style required to harvest the alpha opportunity in the markets was evolving—that we were seeing different types of opportunities emerge.

By 2004, the dust had settled from the tech bubble bursting, and a lot of businesses that were left by the wayside were quietly building real, durable moats. We were seeing real momentum in what would then become, as I like to call it, the pre-smartphone Internet age.

Google was going public, and it was this mysterious, somewhat misunderstood company with a funny IPO prospectus that talked about “don't be evil” and ran a Dutch tender IPO pricing mechanism. Nobody really knew how to think about it.

If you remember, at the time, the entire business model was completely novel; the idea that you could monetize search using advertisements for keywords was completely unheard of.

When I went to interview with Brett, it was clear instantly that he was thinking about things completely differently than at my firm at the time. It was all really about having a growth mindset—trying to look at what the earnings in the next two years were most likely to be.

At the time, a lot of people looked at these businesses as incredibly speculative, trading at very high multiples of what you could see in current earnings. But the art was in being better at predicting what was around the corner.

I know it sounds very obvious as I explain it, but at that time, this was a very provocative way of thinking about it. And it wasn't just Google; it was eBay, it was Amazon, it was Apple, it was Research in Motion—which is no longer the company it once was.

But these were the types of opportunities at that time. They were highly controversial because these business models were very nascent—or maybe didn't really exist at all. So, you had to have the imagination and the foresight. And then, of course, do the deep work and research to understand.

That mindset very much attracted me to Tremblant.

I'm a little hesitant to ask this because we might get ourselves down a wormhole… but how do you compare today's environment to the tech bubble? Is it time to be a deep value investor again?

MC: Of course, there are parallels whenever you're in the midst of what I would call an investing super cycle. There is always a risk of overbuilding, and some amount of overcapacity will have to be digested.

As of today, we do not see that as being a problem. Now, at some point in the future, could that become a problem? Absolutely. But, as of today, we do not see a bubble. There are two major differences that I would flag:

Number one, the level of investment as a percentage of GDP and profits is materially lower than it was in the ’98–‘99 time frame—what I'll just call the fiber overbuild period.

Number two, the use of balance sheet financing looks completely different. Today, it's mostly equity-financed, rather than vendor-financed. I think that's a major, major difference.

Also, you're seeing tangible returns on invested capital and productivity gains that are supporting the investment levels, which were pretty much absent in the ‘99 time frame. Back then, it was much more of a Field of Dreams scenario; we’ll build all this capacity, and all these businesses will eventually come and absorb it.

Today, you're seeing that any compute and power brought online is used instantly, and customers are seeing tangible returns on invested capital.

Meta (Facebook) is probably the biggest and easiest example of where they're leveraging a lot of this compute and more sophisticated AI to drive improvements in their ad algorithm and engagement, which has not only enhanced their revenue growth but also their profitability.

That's probably the most obvious business-to-consumer example, but we're seeing this across a number of smaller companies as well.

Okay. Let’s bring the conversation back to Tremblant. What are your core investment beliefs that you rely on to try to beat the market?

BB: When we look at a company, we want to understand its competitive advantage and whether it is sustainable over time. Similarly, when we look at ourselves, we ask what our competitive advantage is. Why is it sustainable over time?

Number one, we have a process that’s deeply rooted in fundamental research. Number two is our people. Number three is our time horizon.

The amount of short-term trading around stocks is just amazing to me. I'll give you one example I've been dealing with for the last few weeks.

We own a stock called Wingstop. We think it's a fantastic business model and a fantastic financial model—it's a franchisee system. We love franchise business because there's very little capital expenditure (CapEx). They don't own the restaurants; they franchise them to people who run them and pay a fee.

The stock has bounced over the last three weeks between $220 and $280, up and down. It's not moving 20% every day, but over three to five days it's down 20%, then up 20% over the next three to five days, and then down again.

So that's the type of thing we see. But our competitive advantages—process, people and time horizon—are about being able to look out on the horizon and not get distracted by these volatile moves intraday or intraweek.

Lastly is depth of research. By the time we get involved in something, we like to think we know it better than other people. In many cases, over the years, we've come across stuff where we know certain aspects of their business even better than management does, thanks to our competitive analysis. That helps us make decisions.

If you're day trading a bunch of stocks, it's harder to do really deep research on them.

On your website, the investment process centers around companies undergoing “consequential change.” Can you discuss two stocks undergoing consequential change—one that's about change at the company and then one that's more about change in the industry or in the world?

MC: I’ll illustrate this in a company that is a major investment for us currently: Lumentum, whose ticker is LITE—it’s very topical for the AI buildout that's happening right now.

I use the term super cycle because we're in the process of building a tremendous amount of compute that will be needed to get to higher levels of artificial intelligence. It's a simple engineering challenge. How can we increase the amount of computing power inside a data center?

Well, we can just build a bigger data center and put more and more graphics processing units (GPUs) and more and more racks inside. But that requires more power, more space, more cooling, more money. At some point, that becomes an inefficient method of scaling computing power.

The solution is optical and lasers swapped in exchange for copper [wires]. What that allows you to do is scale up the computing power of a given cluster of GPUs.

To use a very simple modular example, if I connect 8 GPUs with lasers so that they can all communicate with one another, well, now I've massively enhanced the amount of computing power versus a scenario where those eight GPUs cannot talk to each other.

So, why is this interesting?

Because lasers happen to be very difficult to make. There are really only two companies in the world that can make them to the spec that is required for this kind of implementation. There’s Lumentum, and the second competitor is somewhat down the quality curve in our view.

So we've done the work to build conviction that we have identified a critical, consequential change and a company that has what we believe is a durable moat. We then moved to try to quantify the financial impact on this business and whether or not it is properly understood in the market.

By moving to co-packaged optics, we're talking about anywhere between 3 and 10 times the number of connections required in a data center. So, you have a business in Lumentum with $3 billion in revenue today, at stage one. Increasing the number of connections by three times will add $3 billion in revenue to the business. And in the final stage, at 10 times the number of connections, we're talking about another $10 billion of revenue to the company.

So it's a business that's doing $3 billion in revenue today, and we believe they'll be doing somewhere between $7 and $10 billion within the next five years. And two years beyond that, between $10 and $15 billion. That translates into $40 in earnings per share in the next three years and $60 to $70 in five years. If you look at consensus estimates, we're roughly double those numbers.

That’s an example of identifying a change that impacts this company in a very consequential way. And then our estimate of the company’s earnings power is materially ahead of the consensus. Then we put a multiple on those earnings to understand whether or not it's still an attractive financial return profile, which we believe it is.

That's how I would summarize our investment process.

BB: Basically, we’re looking at the future and saying we think the future is different than other people.

Very big picture: what we've observed, particularly in consumer or human behavior, is that there's a “tipping point.” Malcolm Gladwell wrote The Tipping Point in 2000, where he pointed out that people adopt things faster or let go of things faster than everybody realizes.

We can give lots of examples of that over the last few decades.

Just looking at the Vanguard portfolio, Uber brought in Dara Khosrowshahi. He was the catalyst that made Uber more interesting to us because they brought in a professional to clean up the company and focus it on economic returns and cash flow. And he's done an amazing job of that. Now he's got a different challenge with autonomous vehicles, but we continue to think there will be a central hub for that, and that will be Uber.

Chipotle and Starbucks are both in the portfolio, and both brought in new CEOs in the last 12 months. We think they're both doing a really good job cleaning up what was a bit of a mess.

I’ll quickly discuss two of my favorite historical examples:

One is Royal Caribbean, which is now in the Vanguard portfolio. Many years ago, they hired a new CFO, which is not usually something to get too excited about. But we took a meeting and asked why he left another big job to go there. What do you see as the opportunity?

I'm paraphrasing, he said, the way I look at the company is, 10 years ago, we earned $2.00 in EPS, and over the next 10 years, we spent $3 billion building new ships. And this year we're going to earn $2.00 in EPS. Something's wrong with that model.

So the new CFO said, to take the job, I got the board to agree that we're going to evaluate all senior management on increases in returns on invested capital—that is the most important metric and should be the mission of the company.

We thought, oh man, this is awesome. He's exactly right.

That is a great example of when someone comes in with a new financial strategy or focus and changes the company.

The last example I'll use is Amazon. Many years ago, Amazon would buy—I'll use toothpaste as an example—they’d buy pallets of toothpaste. Then you or I would go on the Amazon website and order some toothpaste, and they'd send it to you.

But over time, Amazon moved to a different model:

First, the manufacturer would put their toothpaste in Amazon's warehouse. Amazon doesn't buy the toothpaste; it's held for the manufacturer. Amazon just ships you a tube of toothpaste, takes your money, keeps 15% and gives the rest back to the manufacturer.

The third level is even better. You go to the website, order the toothpaste, and the order is sent to Amazon. Amazon doesn't hold the toothpaste; they route the order to the manufacturer, who then sends you the toothpaste directly and sends Amazon a percentage of the revenue.

Of those three ways of fulfilling your order, the latter two have much higher return on invested capital (ROIC) for Amazon.

Let’s take Starbucks as an example. Everybody knows they have a new CEO who's trying to do something new—that’s not “new” information. But, in effect, you’re saying, “I think the market is underappreciating the impact that the new CEO is going to have on the company. We have a variant view of what the impact is going to be.” Is that a good way to think about it?

BB: Yeah, that is correct. But there's a lot that goes behind it in terms of independent research.

For example, years ago, when Starbucks would launch new products—like the cheese and chive scone—they would get two things wrong.

One, the old management started advertising it before it was available on the shelf. So marketing 101 is you wait till the product's available, then you advertise it to drive people into the store. Advertising in advance is wrong-minded because it sets people up for disappointment.

The second issue was that it wouldn't be available either because it wasn’t in stock or hadn't been delivered—and that's maddening to the consumer.

I saw the ad for the scone, and I really want it. I come into the location, yet I can’t get it. Now I'm upset as a consumer.

So, when speaking with management about these simplified examples, we asked, "What are they focused on?" The consumer experience? Simplifying the menu? Making sure that the core new launches are available when they're rolled out?

Now we can do independent research to track that kind of stuff, which we do very well. It's not hard for us to create a web bot that goes out and tries to figure out if a product is available at these 50 locations or these hundred locations. We can do all that now pretty seamlessly and simply, thereby proving whether the new CEO at Starbucks, for example, is doing what he said he's going to do.

And then we can project the cash flows they will generate into the future and discount them back to today. What's that resulting value? Is it materially different than where the stock is trading?

We can test whether they’re getting the execution right with independent research. We can prove out that our earnings estimates—whether for Starbucks or somebody else—are on target.

MC: To augment what Brett's saying, I believe that this is probably one of the areas, at least today—and hopefully it proves durable—where active managers can continue to add significant alpha.

If you think about just the sheer volume of shorter-term trading strategies—whether it's multi-manager funds and statistical arbitrage-type quantitative program trading platforms—which use enormous amounts of data and algorithmic computing. We're not trying to compete in that short-term alpha capture game.

With the explosion of information and data that's available, I think there's real value in human judgment and experience in knowing what actually matters—being able to filter some of the signal from a lot of that noise.

A real-world example is our experience with food delivery platforms like DoorDash.

Now, a lot of people are tracking credit card spending data, which will give you a picture of overall orders and has a pretty high correlation with revenue. However, it tells you very little about what the actual profitability of the business is going to be. Why? Because there are lots of ways that you can give away discounts, credits and other things. You can stimulate a lot of revenue, but it might be a very unprofitable business.

We determined, through researching the businesses and having real-world conversations with management teams, that Dasher (delivery person) wait time was a key metric for understanding whether the logistical network was functioning well. And it had a very high, direct correlation with profitability and EBITDA margin.

Think about it in a real-world situation. If the dasher shows up at the restaurant and has to wait 30 seconds versus 3 minutes, that is going to translate into a more satisfied customer. You're getting your food on time. That means it's not cold. That means there won't be any credit or refund due to a customer complaint. And that Dasher, by saving time, will make more deliveries for DoorDash, which translates into enhanced profitability.

So we were able to filter out a lot of the noise—we were able to suss out what we thought actually translated into real-world performance.

By looking not just one quarter out but, as Brett has talked about, 6 to 18 months out—which we think is the sweet spot of alpha capture for our strategy—and projecting what we thought the business’s earnings power would be, we saw a significant difference between our view and the consensus. That to us was an actionable idea.

Thanks. That's a good sense of how you guys think about picking stocks, but then you do have to translate that into a portfolio. So how do you think about constructing a portfolio of companies undergoing consequential change?

BB: We're wired to be looking for the best ideas, but we're trying to solve for how to implement these best ideas within our risk budget. Whether it's the Vanguard portfolio or any portfolio we manage, we agree on the rules of the road and then we have to stay within those lines.

We have a robust risk engine that we built over the 25 years we've been in business. We have hourly risk reports and weekly risk meetings. We also have an independent third-party advisor who has worked with us for at least 15 years, and reviews all of our risk numbers every night to see if there's any issue.

We talk it through with him constantly, but risk management focuses on the quality of the return. We don't want one or two individual investments to drive all the return. We want to have a high hit rate.

And the best way to do that is to do good work on a string of ideas, and then make sure that there's no factor or unintended risk that you're not thinking about.

All knowledge falls into three buckets. You know what you know, and you know what you don't know. But it’s the third bucket that terrifies us; what do we not know that we don't know?

And so we're constantly trying to solve for that to make sure that nothing's going to bite us that we're not thinking of.

MC: The Vanguard MidCap Growth fund should have 45 to 60 total investments in the portfolio at any given time—that will fluctuate depending on the opportunity set and our conviction level. Generally speaking, each position will be anywhere between 1% and 3% of the portfolio.

We strive to keep the tracking error between 5% and 9%. We are very factor- and sector-aware. Sector awareness is pretty obvious, just looking at where the benchmark is in terms of its overall composition versus where our actual managed portfolio is.

All of our investment professionals are very aware of everything in the benchmark that is above 50 basis points and must have a point of view on those names.

And certainly any position in the benchmark over 1%, to the extent that we are not going to own it, we're effectively short it—our background in hedge funds has really given us a good framework for thinking about what that means, and how we want to manage that sort of risk.

And so hopefully that gives a flavor of how we're attacking this, but I think the risk factors in the market are very dynamic.

The new risk factor became “AI winner, AI loser, or other.” It was very clear that, in January and certainly in February, this became a risk factor you needed to overlay on your understanding of how your portfolio was behaving.

And so we did the exercise of tagging every one of our positions in the Vanguard portfolio to one of those three buckets. Is the market treating this as an AI winner, an AI loser, or “other”—which we would call other/defensive?

That really gave us a good feel and an awareness of where the risk in the portfolio was and whether we were positioned the way we wanted to be.

At times, we may choose to increase our level of active exposure because we think the opportunity set is so rich, which would likely put us at the lower end of that 45 to 60 name band. The average position size might creep up. The tracking error may creep up a bit, but we will certainly strive to keep it within that band.

Again, that's all part of a deliberate, intentional strategy driven by our very high conviction in the opportunity set.

To put this in my own words: You're trying to build a portfolio that is midcap growth, but will be driven by the names that you guys have conviction in and have done your deep research on. Is that a fair summary?

MC: 100%

BB: Bullseye.

Great. I don't necessarily want to spend a ton of time on your global ETF (TOGA), but is it fair to think of that as a place where the rules of the road are wider—where you're willing to accept more tracking error?

BB: Yes, TOGA’s very separate from the Vanguard portfolio we manage. It's completely different. It's index agnostic. It's the best ideas, more opportunistic, less constrained—whether geographic or other things. It's global, more than 1/3 of it right now is non-U.S.

So it's quite different.

Okay. Sticking with the Vanguard funds, in terms of setting expectations: Are there certain environments where your strategy tends to perform relatively well or relatively poorly?

For example, Vanguard Dividend Appreciation Index owns dividend growers, which are typically big, stable, defensive companies. The fund tends to lag in bull markets but to do relatively well in bear markets.

Are there environments where I would expect Tremblant to really be running? Or that some environments might provide more of a headwind?

BB: 25 years later, one thing we've learned about ourselves is that when the market is slowly drifting upwards to the right, it can be harder for us to generate outperformance.

But what happens when markets get volatile, as they just did over the last eight weeks? Typically, we underperform the broad market index.

But coming out the other side, we tend to perform very well.

Why?

Because when things get hairy, investors—be it retail investors getting margin called or multi-manager hedge fund shops cutting risk really quickly—prices get blown all over the place. In the moment, we'll get dinged up by that. But if we do our job right, we set ourselves up very well for thereafter.

That's how we feel right now with the volatility that we've experienced so far this year. As Michael said, there are AI winners and losers. But we'll see over the next 6 to 12 to 18 months the decisions we're making now and the things that we're buying and the things we're selling, how that will perform.

But, usually, we do very well on the other side of market dislocations.

MC: Exogenous shocks produce market dislocations, which tend to have very high correlations. When all assets become very highly correlated, that—in the 25 years that we've been doing this—has been an alpha-rich moment of opportunity.

I can talk about the most recent one in January and February, which I'm calling the Claude event. It was an exogenous shock to the market because you saw multiple sectors become highly correlated. We believe that it won't sustain and will become the source of alpha.

Or, think back to early 2020: COVID was an exogenous shock with extreme dislocation and very high correlation. It was an alpha opportunity for us. A number of businesses and companies traded in a distressed manner for understandable reasons. But very quickly it became clear that there would be winners and losers in that environment, which created the opportunity.

We see the same thing today.

Thank you for your time today. Before I wrap up, what should a new investor in MidCap Growth and Tremblant Capital know that we haven't covered?

MC: The mid-cap growth space is a tremendously alpha-rich area of opportunity.

In today’s investment landscape, there is so much less focus on this area by active managers, which is understandable. The top of the market is dominated by some world-class companies that are growing at tremendous rates. It's something that we've never seen before. And so there are sufficient capital deployment opportunities for the large pools of capital to execute their strategies that they don't need to focus on the tremendous number of companies that are in the mid-cap growth space.

What I've come to realize really is that there is a tremendous opportunity for outperformance in this area, given the market dynamics and lack of focus. As an investor, I would say it's an excellent area to focus on.

BB: I like Michael's answer, but I can't resist the temptation to just throw it out there—and everybody rolls their eyes—but the broader indices are so top-heavy with multi-trillion-dollar companies.

I agree with Michael. These companies are the best in the world. They generate tons of cash, and they're growing rapidly. But doubling or tripling your money on a $3 to $5 trillion market cap is a lot tougher than us finding a company in the $25-$50 billion market cap zip code.

Finding things there that can compound for 3, 5 or 10 years is just mathematically more attractive to me.

Vanguard and The Vanguard Group are service marks of The Vanguard Group, Inc. Tiny Jumbos, LLC is not affiliated in any way with The Vanguard Group and receives no compensation from The Vanguard Group, Inc.

While the information provided is sourced from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Additionally, the publication is not responsible for the future investment performance of any securities or strategies discussed. This newsletter is intended for general informational purposes only and does not constitute personalized investment advice for any subscriber or specific portfolio. Subscribers are encouraged to review the full disclaimer here.