Hello, and welcome to the IVA Weekly Brief for Wednesday, April 15.

There are no changes recommended for any of our Portfolios.

At the start of April, after a 5.0% drop in March, I told you that buying stocks after a sharp one-month decline tends to work out more often than not.

With 500 Index (VFIAX) up 6.8% so far this month and Total International Stock Index (VTIAX) up 7.6%, that call is looking prescient, at least in the short term.

But let me be clear: I wasn’t thinking about the next 12 trading days—I was thinking about the next 12 months. I’m not a short-term trader, and I wasn’t trying to call a market bottom. That’s a fool’s errand.

The idea was much simpler. Every correction—and every bear market—eventually gives way to a bull market. History tells us that putting money to work after a meaningful decline has generally been a profitable move.

If you need another concrete example, consider what I call the “3.5% Solution.” (Not really a “solution,” but a useful rule of thumb I picked up from my mentor.) He found that buying stocks after a one-day drop of 3.5% or more tended to produce strong forward returns.

The numbers back it up: Buying 500 Index on those big down days led to an average 12-month return of 24.6%.

We had a real-time test last year. On April 3, 2025, 500 Index fell 4.8%. The next day, it dropped another 6.0%. Not exactly comfortable buying conditions.

But what happened if you stepped in?

If you bought on April 3, your return over the next 12 months was 20.3%—despite being down 6.0% immediately. If you bought on April 4, your return was 27.9%. For context, 500 Index has compounded at 10.8% annually over the past four decades.

Sharp declines are unsettling, but for investors willing to stay the course (and occasionally lean in to market drops), history suggests those uncomfortable moments are often where the opportunity lies.

Foreign Growth and Value ETFs Arrive

After hitting snooze once, I expect Vanguard will launch Developed Markets ex-U.S. Growth Index ETF (VDG) and Developed Markets ex-U.S. Value Index ETF (VDV) this week.

Premium Members can read my full take on these ETFs—and how they stack up against Vanguard’s legacy actively managed funds—here.

An Unexpected Display

Owners of Treasury Money Market (VUSXX) may have noticed an unusual note at the top of their March statements:

"Your March 2026 VUSXX dividend was paid as expected but will not appear on your March statement. The dividend and its reinvestment will be reflected on your April statement, and the total dividend was not impacted."

Vanguard assured me that “investors received their March dividends on the normal schedule, with no impact to their investments.” That’s good. So, on the face of it, it’s business as usual.

But the firm also acknowledged that “the transactions weren’t displayed as expected” and that a “one-time posting delay caused the March dividend for VUSXX to appear on April month-end statements instead of March.”

In other words, the money is there, but the plumbing to the account statement didn’t quite work.

This appears to be a one-off issue, and I haven’t seen similar problems reported for other funds. Still, it’s a reminder that even the most routine processes at Vanguard aren’t always as seamless as they should be.

After all, reporting a money market fund’s monthly distribution should be about as straightforward as it gets. Vanguard has done it thousands of times over the past five decades.

And yet—here we are.

A Vanguard Debit Card?

A tip of my cap to Joe Morris at Ignites for catching this:

Vanguard recently hired Adam Gill as Director of Debit Card & Money Movement, according to LinkedIn. His mandate? “Work with the Cash & Savings team to launch debit card and modernize money movement capabilities.”

Read between the lines, and it’s not hard to see where this is headed. A debit card—and possibly checkwriting—could be coming to Cash Plus Account.

That would be a welcome development. As I’ve said before, the lack of an ATM card and checkwriting has been a dealbreaker for me with Cash Plus. If Vanguard closes those gaps, Cash Plus starts to look a lot more like a complete cash offering—not just a savings account with a few bells and whistles.

More PRIMECAP ETF News

Following up on last week’s news that a PRIMECAP-managed ETF is in the works, the firm has taken the first formal step—submitting an application to the SEC—to offer ETF share classes of its existing Odyssey mutual funds.

Premium Members can read my full take on the dual mutual fund–ETF share class structure here. The pitch is straightforward: Adding an ETF share class could make these legacy mutual funds more tax-friendly. But the reality is less certain.

This structure hasn’t been fully tested, and a key question remains: Can a relatively small ETF sleeve meaningfully chip away at the large, embedded gains sitting in the mutual fund? I can’t answer that with full confidence.

In other words, don’t assume that an ETF share class automatically means the end of capital gains distributions. If PRIMECAP adds an ETF sleeve to, say, PRIMECAP Odyssey Aggressive Growth (POAGX), the fund’s distributions may or may not disappear overnight.

In short, I’d like to see the dual share class structure in action before giving the “all clear.”

One final note: This filing applies to PRIMECAP’s private-label Odyssey funds—not its Vanguard funds. We may eventually see Vanguard ETFs run by PRIMECAP Management, but for now, PRIMECAP (the company) is moving ahead on its own.

Our Portfolios

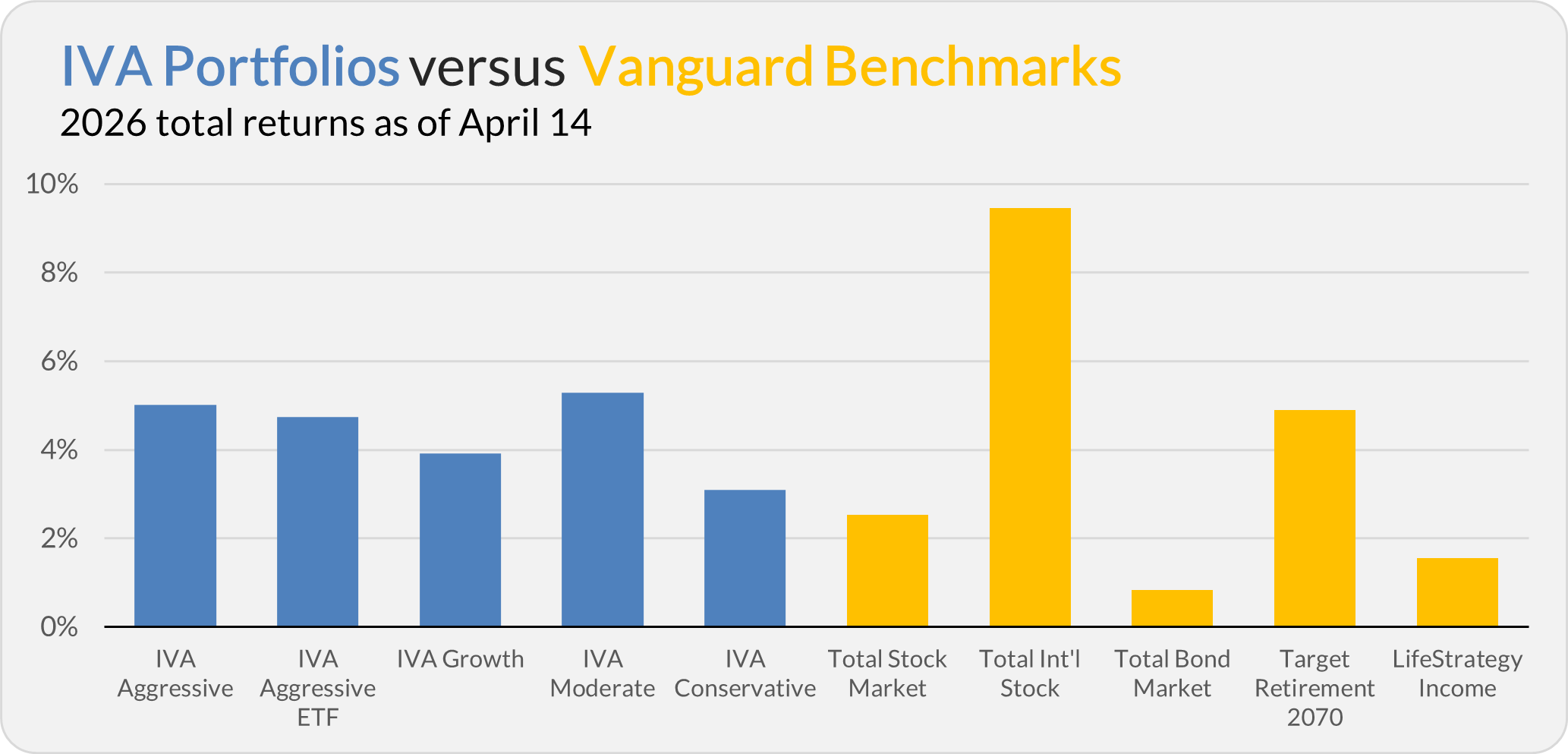

Our Portfolios are showing positive returns for the year through Tuesday. The Aggressive Portfolio is up 5.0%, the Aggressive ETF Portfolio is up 4.7%, the Growth Portfolio is up 3.9%, the Moderate Portfolio is up 5.3% and the Conservative Portfolio is up 3.1%.

This compares to a 2.5% gain for Total Stock Market Index (VTSAX), a 9.5% return for Total International Stock Index (VTIAX), and a 0.8% gain for Total Bond Market Index (VBTLX). Vanguard’s most aggressive multi-index fund, Target Retirement 2070 (VSNVX), is up 4.9% for the year, and its most conservative, LifeStrategy Income (VASIX), is up 1.5%.

IVA Research

Yesterday, I answered a common IVA reader question: Can I follow the Portfolios in a taxable brokerage account?

Until my next IVA Weekly Brief, have a safe, sound and prosperous investment future.

Still waiting to become a Premium Member? Want to hear from us more often, go deeper into Vanguard, get our take on individual Vanguard funds, access our Portfolios and Trade Alerts, and more? Start a free 30-day trial now.

Vanguard and The Vanguard Group are service marks of The Vanguard Group, Inc. Tiny Jumbos, LLC is not affiliated in any way with The Vanguard Group and receives no compensation from The Vanguard Group, Inc.

While the information provided is sourced from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Additionally, the publication is not responsible for the future investment performance of any securities or strategies discussed. This newsletter is intended for general informational purposes only and does not constitute personalized investment advice for any subscriber or specific portfolio. Subscribers are encouraged to review the full disclaimer here.