Hello, and welcome to the IVA Weekly Brief for Wednesday, May 6.

There are no changes recommended for any of our Portfolios.

Let’s take stock of the economy by looking at the “big three” metrics—inflation, unemployment and Gross Domestic Product (GDP):

Inflation is running hotter than the Federal Reserve's 2% target—as it has for years—and the war with Iran isn't helping. Consumer prices, measured by the Consumer Price Index (CPI), are up 3.3% over the past year. Worryingly, prices rose at a 5.3% annual pace in the first quarter.

The Fed's preferred inflation gauge—core PCE—tells a similar story, up 3.2% over the past 12 months and running at a 4.4% annual pace in the first three months of the year.

The labor market looks fine on the surface. Unemployment has held steady in the 4.3%–4.5% range for eight months running. But job creation has dried up—a concern tempered somewhat by the fact that the labor force itself isn't growing much, as immigration slows and older workers retire. Call it an uneasy equilibrium.

The U.S. economy grew 0.5% in the first quarter after inflation. In dollar terms, real GDP—that is, GDP adjusted for inflation—rose $120 billion to a record $24.2 trillion. Annualized, that 0.5% quarterly gain works out to 2.0% growth—right in line with the average over the past two decades.

The bottom line: The economy has been incredibly resilient—absorbing tariff disruptions without slipping into recession—but it's not exactly growing by leaps and bounds. Oh, and inflation continues to run a bit hot.

That's the environment Kevin Warsh is inheriting as he prepares to take over as Fed Chair on May 15. I don't envy his position.

Warsh and his fellow policymakers face some genuinely tough questions: Do they "look through" the inflationary impact of rising oil prices? How much can they rely on artificial intelligence to boost productivity and bring inflation down? What do they make of a steady unemployment rate paired with stagnant job creation?

Tough questions—and that's before accounting for the pressure coming from the White House. That pressure has led current Fed Chair Jerome Powell to make an unusual decision: staying on the board after his term as chair ends.

The distinction matters. A Fed chair's term runs four years; board seats last 14. So while Powell's chairmanship is up, his board seat runs through 2028. Normally, outgoing chairs step down from the board entirely to avoid any perception of a shadow chair or power struggle. Powell has decided that staying is the better way to defend the Fed's independence.

Agree with him or not, that's the reality. And as investors, we have to deal with the world as it is, not as we might want it to be.

So, what are we, as investors, to make of all this?

Start with rates. With inflation still running above the Fed's 2% target, the most likely path for interest rates is sideways—higher for longer, or at least on hold for longer.

That matters for how you think about cash versus bonds.

Federal Money Market (VMFXX) is currently yielding around 3.57%. That’s short of Total Bond Market Index’s (VBTLX) 4.35% yield—but to earn that extra yield, you're taking on meaningful interest-rate risk. For now, cash continues to earn a respectable return without the volatility.

That said, don't let the Fed headlines push you to the sidelines on stocks.

No, the economy isn't growing by leaps and bounds. But 2% real growth isn't a recession—it's a continuation. Companies are still earning, consumers are still spending and the labor market, whatever its flaws, hasn't cracked. That's not the backdrop for a dramatic repositioning out of stocks.

The message is the same one I keep coming back to: stay invested, stay diversified.

A New Website Is (Finally) Coming

Vanguard CEO Salim Ramji published his latest annual letter this week. Long may this tradition continue.

The headline item for most IVA readers will be this: Ramji says Vanguard is "near completion of a multiyear, multibillion-dollar investment to modernize its technology infrastructure," and a refreshed website is coming in the next few months.

That's welcome news. I haven't been shy about criticizing Vanguard when it's fallen short on service and technology. But I've also said I can't wait to cheer when they right the ship. Hopefully, that moment is drawing near.

The website isn't all that Ramji is promising. The firm is expanding chat capabilities through artificial intelligence, increasing the number of trained service representatives by 20% and—this one will resonate with longtime readers—bringing back a more personalized service tier for Flagship investors. Flagship status hasn't meant what it used to in recent years. It's good to see Vanguard acknowledging that.

On the product side, Ramji said more actively managed bond funds and enhancements to Cash Plus Account are on the way. I'll keep you posted on both as the details emerge.

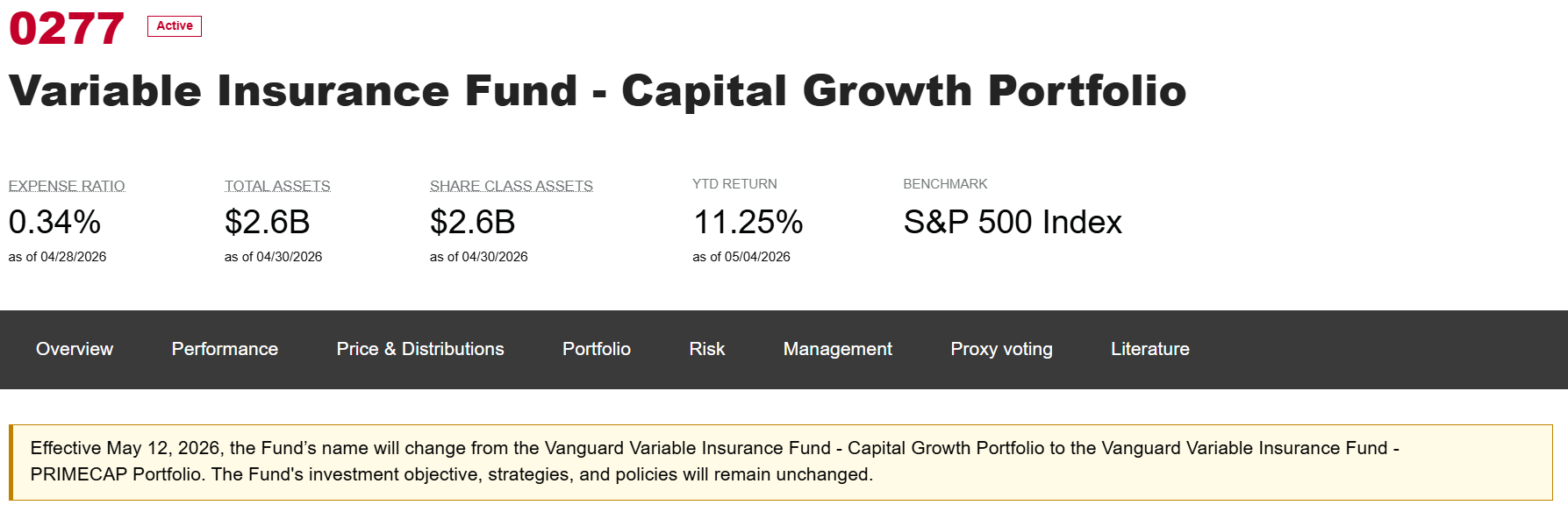

Another Name Change, Nothing More

A quick heads up: This time next week, Capital Growth Annuity will be renamed PRIMECAP Annuity.

Only the name is changing. The managers, strategy and everything else are staying the same. All this does is clearly indicate to Vanguard investors that Capital Growth Annuity is the same as the PRIMECAP (VPMCX) fund—only in an annuity wrapper.

Donor-Advised, Not Donor-Controlled

A few weeks ago, I wrote to you about Vanguard Charitable—one of the nation’s largest donor-advised funds (DAFs). It was back in the news last week after blocking grants to the Southern Poverty Law Center (SPLC).

Vanguard Charitable—a nonprofit public charity technically separate from Vanguard, the investment firm—has a policy that if “a nonprofit organization has been charged by regulatory authorities for criminal activities that call into question its ability to carry out its charitable purpose, [it] may deny the grant.”

After the Justice Department indicted the SPLC, Vanguard Charitable stopped making grants to the civil rights nonprofit. Fidelity Charitable reached the same conclusion, though other DAFs—like Daffy—have not.

Reasonable people will disagree about whether blocking grants before a case is resolved is the right call. But here’s the practical reminder:

Vanguard Charitable (like all other DAFs) is a donor-advised fund—emphasis on advised. Vanguard Charitable generally follows your guidance on how to invest the assets and where to direct them. But once you've funded your account, the nonprofit becomes the legal owner of those assets and has the final call.

That doesn’t mean you shouldn’t give to a DAF. It means you need to be aware of the trade-offs.

Our Portfolios

Our Portfolios are showing solid returns for the year through Tuesday. The Aggressive Portfolio is up 8.0%, the Aggressive ETF Portfolio is up 7.4%, the Growth Portfolio is up 6.8%, the Moderate Portfolio is up 7.9% and the Conservative Portfolio is up 4.5%.

This compares to a 6.8% return for Total Stock Market Index (VTSAX), a 10.5% gain for Total International Stock Index (VTIAX), and a 0.1% return for Total Bond Market Index (VBTLX). Vanguard’s most aggressive multi-index fund, Target Retirement 2070 (VSNVX), is up 7.5% for the year, and its most conservative, LifeStrategy Income (VASIX), is up 1.7%.

IVA Research

Yesterday, I took a hard look at Vanguard's factor ETFs—and found that eight years in, they haven’t quite delivered on the promise of market-beating returns.

Until my next IVA Weekly Brief, have a safe, sound and prosperous investment future.

Still waiting to become a Premium Member? Want to hear from us more often, go deeper into Vanguard, get our take on individual Vanguard funds, access our Portfolios and Trade Alerts, and more? Start a free 30-day trial now.

Vanguard and The Vanguard Group are service marks of The Vanguard Group, Inc. Tiny Jumbos, LLC is not affiliated in any way with The Vanguard Group and receives no compensation from The Vanguard Group, Inc.

While the information provided is sourced from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Additionally, the publication is not responsible for the future investment performance of any securities or strategies discussed. This newsletter is intended for general informational purposes only and does not constitute personalized investment advice for any subscriber or specific portfolio. Subscribers are encouraged to review the full disclaimer here.