Hello, this is Jeff DeMaso with the IVA Weekly Brief for Thursday, June 20.

There are no changes recommended for any of our Portfolios.

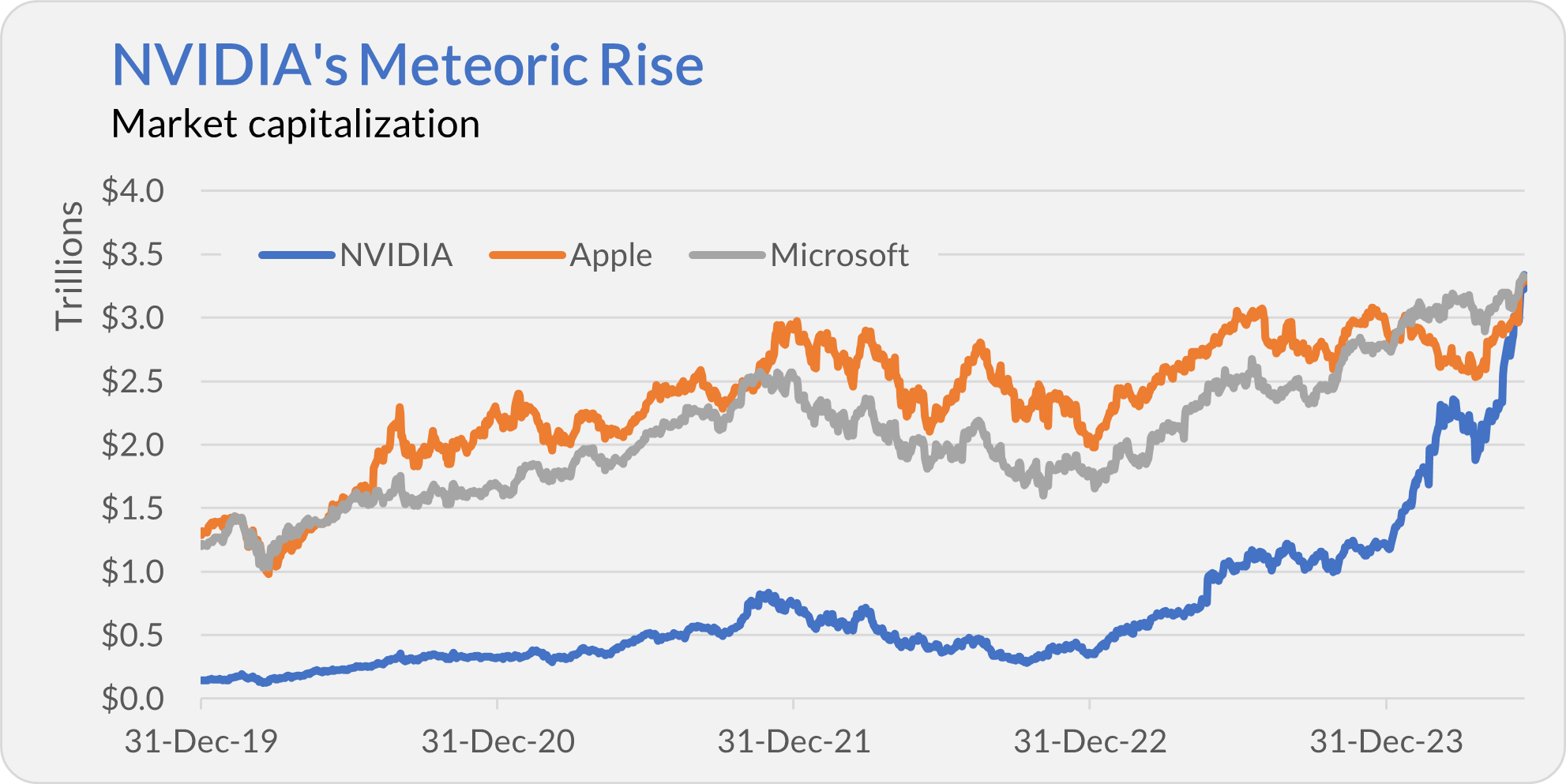

As if out of nowhere, artificial intelligence (AI) and the companies that support its existence are driving the stock market to new highs. To wit, on Tuesday, NVIDIA—the company that makes the chips that enable AI—became the largest company in the U.S. (and the world) by market capitalization (size), worth more than $3.3 trillion.

Apple and Microsoft have been vying for the crown for several years, but NVIDIA’s rise to the top has been astounding. Since ChatGPT’s launch at the end of November 2022, NVIDIA’s stock has risen 8-fold, from a little over $400 billion in size to over $3.3 trillion.

I know some people are feeling WIBI (Wish I’d Bought It) syndrome, but frankly, I don’t think NVIDIA’s run is sustainable. Also, don’t kick yourself too hard—NVIDIA was virtually unknown, and its stock was doing nothing just a few years ago.

However, I wouldn’t say NVIDIA was completely unknown. Consider that the stock pickers at PRIMECAP Management first bought NVIDIA’s stock in PRIMECAP’s (VPMCX) portfolio sometime between September 2009 and March 2010! And yes, they still own the stock.

PRIMECAP’s Doors Are Open

Speaking of the PRIMECAP team, as I told Premium Members on Tuesday, Vanguard has reopened PRIMECAP and PRIMECAP Core (VPCCX) to investors for the first time in roughly two decades. (Technically, PRIMECAP has been closed since 2004, and PRIMECAP Core has been closed since 2009—though existing investors could add limited amounts to their stakes.) Vanguard’s other PRIMECAP-run fund, Capital Opportunity (VHCOX), is still closed to new investors.

Now is your chance if you’ve been waiting to buy PRIMECAP or PRIMECAP Core. That said, if you’ve been following my advice, you already have a significant allocation to the PRIMECAP Management team—either through Vanguard’s PRIMECAP-run funds or the private-label PRIMECAP Odyssey funds.

I won’t be buying either of the two reopened funds, but please do not take that as any indication of a lack of confidence or conviction in the funds and the managers. I’m not buying the funds because, as I’ve told you, PRIMECAP Odyssey Aggressive Growth (POAGX) is my single largest holding—I already have a lot of exposure to PRIMECAP's stock pickers.

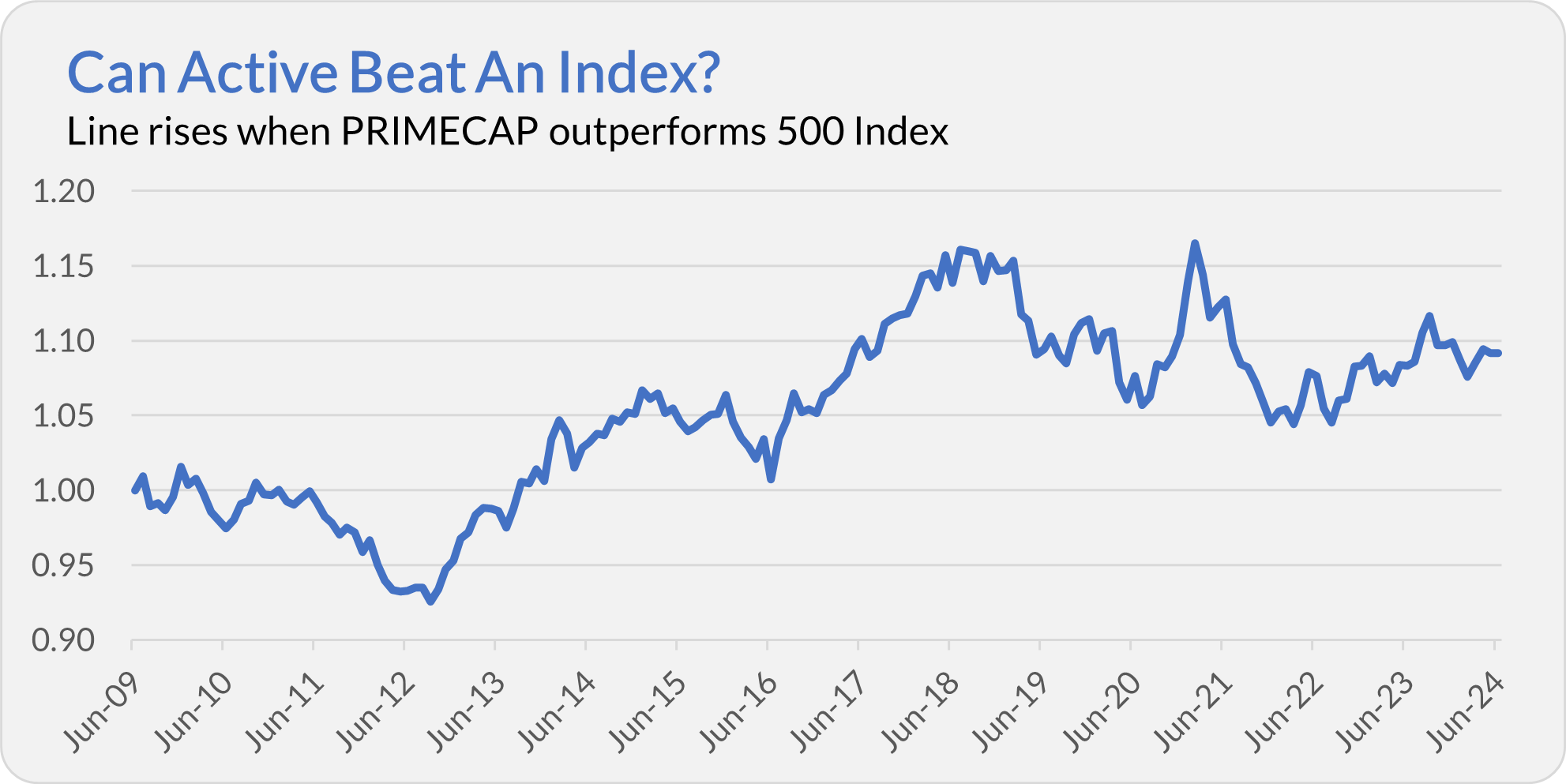

The PRIMECAP team hasn’t exactly been setting the investment world alight lately, but their results are better than you might guess. The chart below shows PRIMECAP’s performance relative to 500 Index (VFIAX) over the last 15 years—the line rises when the active fund outperforms.

Yes, PRIMECAP has trailed 500 Index over the past three years (by around 1% per year). However, the active fund has beaten the index fund over the past five, ten and fifteen years. Who says active can’t win?

Premium members can read more about the PRIMECAP team here. The bottom line is that the PRIMECAP team is among the best in the business. Given that their investment approach is somewhat out of favor, now might be an opportune time to get in.

Outflows in Context

Several IVA readers asked about the large amount of money flowing out of Vanguard’s active mutual funds and if we should be concerned. This recent interview with Morningstar’s Dan Sotiroff sparked the questions. In particular, Sotiroff said:

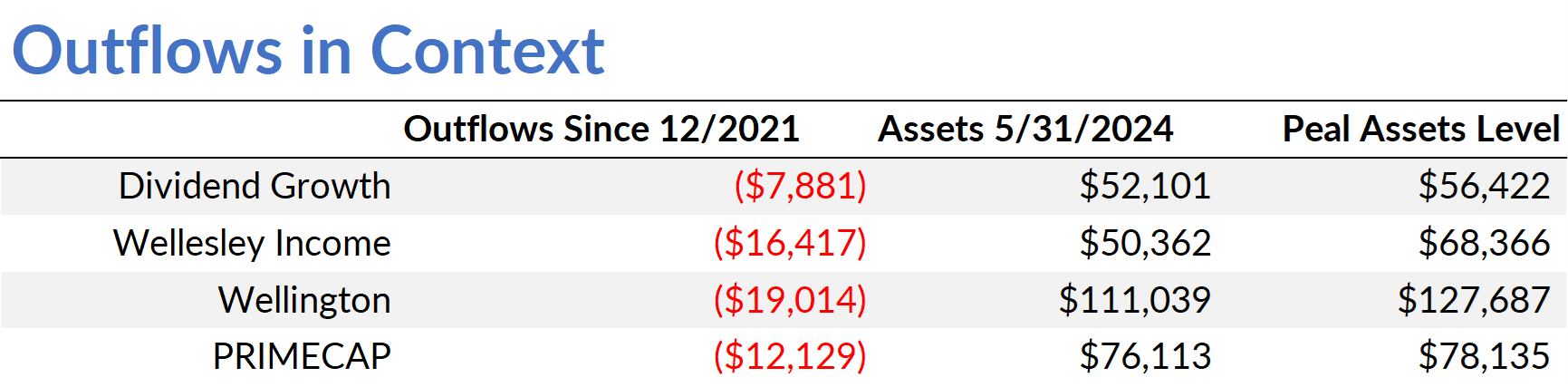

So, if you wanted some specific names: Vanguard Dividend Growth lost about $7 billion over those two years. Wellington, which is kind of a balanced fund, mixed with stocks and bonds, that lost about $15 billion. Wellesley Income lost about $14 billion. And then PRIMECAP, the original PRIMECAP fund from 1984, that lost about $9 billion over the last three years.

He cites some big numbers, but remember that these are also some very big funds. So, let’s put the outflows in context.

The table below shows the net flows from each fund since the end of 2021. (My numbers don’t match Sotiroff’s figures precisely because I’m looking at a slightly different period, but they are substantially similar.) To provide context, I included each fund’s size (as of the end of May) and peak asset level.

Despite the outflows, these remain big funds, and each isn’t far off its peak in assets. This tells me that the funds (and managers) aren’t going anywhere.

Investors should be wary of outflows, as they could lead to significant capital gain distributions at the end of the year. However, that isn’t exactly new news. If you’ve held Dividend Growth (VDIGX), PRIMECAP, or either of the two balanced funds in a taxable account, you’ve always had to keep one eye on capital gain distributions in December—something I help you with yearly!

In the bigger picture, money has been flowing from actively managed mutual funds to index funds (and ETFs) for over a decade—not just at Vanguard but industry-wide. Frankly, many active mutual funds shouldn't exist. (Or, said differently, many funds could disappear, and no one would notice.)

I believe there is still room for active funds in the industry, but as has always been the case, you have to be selective about the funds you invest in.

Which IRAs?

As I told you—here and here—Vanguard sold its small business retirement unit to Ascensus. A few IVA readers asked for clarification on which Vanguard accounts will move to Ascensus in July.

Only three types of accounts are moving: Individual 401(k)s, SIMPLE IRAs and multi-participant SEP-IRAs.

Everything else is staying at Vanguard. So, if you have a single-person SEP-IRA, it stays put. Similarly, if you have a Roth IRA, your account does not move, and the same is true for traditional (or rollover) IRAs. Taxable brokerage accounts are staying at Vanguard, too.

I think some of the confusion stems from SIMPLE IRAs. SIMPLE is intentionally in all caps as it stands for “Savings Incentive Match PLan for Employees.” These plans are for small businesses and differ from your standard, run-of-the-mill individual retirement accounts (IRAs).

Our Portfolios

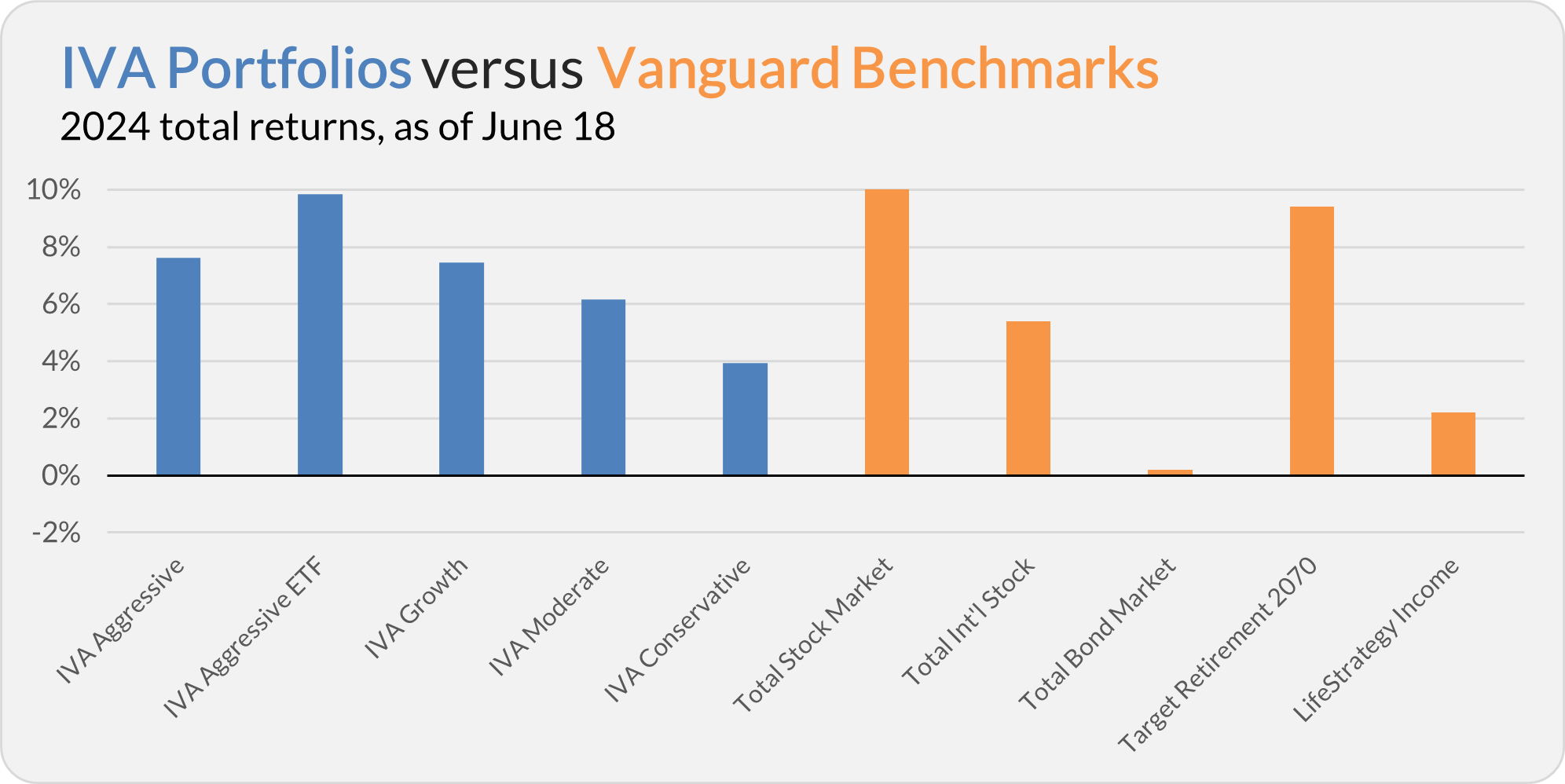

Our Portfolios are showing positive absolute but lagging returns for the year through Tuesday. The Aggressive Portfolio is up 7.6%, the Aggressive ETF Portfolio is up 9.8%, the Growth Portfolio is up 7.5%, the Moderate Portfolio is up 6.2% and the Conservative Portfolio is up 3.9%.

This compares to a 13.9% gain for Total Stock Market Index (VTSAX), a 5.4% return for Total International Stock Index (VTIAX), and a 0.2% gain for Total Bond Market Index (VBTLX). Vanguard’s most aggressive multi-index fund, Target Retirement 2070 (VSNVX), is up 9.4% for the year, and its most conservative, LifeStrategy Income (VASIX), is up 2.2%.

IVA Research

It has been a busy week for IVA readers.

On Monday, I told Premium Members why I’m planning on moving my individual 401(k) to E*TRADE.

On Tuesday, I explained why investors shouldn’t let election-year noise derail a well-considered investment strategy. I also shared the news of PRIMECAP and PRIMECAP Core reopening in a Quick Take.

Until my next IVA Weekly Brief, this is Jeff DeMaso wishing you a safe, sound and prosperous investment future.

Still waiting to become a Premium Member? Want to hear from us more often, go deeper into Vanguard, get our take on individual Vanguard funds, access our Portfolios and Trade Alerts, and more? Start a free 30-day trial now.