Hello, and welcome to the IVA Weekly Brief for Wednesday, March 25.

There are no changes recommended for any of our Portfolios.

War has broken out and disrupted global oil supplies—exactly the kind of shock that, in theory, should send gold prices soaring. After all, gold is often billed as the “ultimate” safe haven and an inflation hedge.

But theory and reality don’t always line up.

Since the conflict began, gold has not risen; it has fallen 16.5%. That’s more than stocks, with Total World Stock ETF (VT) down 6.5% over the same stretch.

A month ago, when I evaluated the case for holding gold in a diversified portfolio, I said investors require “extraordinary discipline.” The past few weeks are a good reminder of why.

Despite what its proponents may say, gold doesn’t behave in a consistent or intuitive manner. Sometimes it rallies in times of stress—other times it doesn’t. Sometimes it protects against inflation—other times it lags badly. If you’re looking for a reliable hedge or a clear pattern, well, rather than glittering, gold has a way of disappointing.

But step back for a moment—this isn’t really about gold.

It’s about what happens when markets wobble, and the news makes you uncomfortable.

An IVA reader wrote in this week with a question that I suspect many of you are grappling with:

"My wife is panicked by the Iran situation and the recent market drop. We’re invested across your Growth and Moderate Portfolios, with a sizable cash cushion, but she wants to move everything to cash and bonds.

We made a similar move during COVID, and it cost us. I think our current strategy still works—but she worries we’re too old to recover from another downturn."

I feel your wife’s pain and your desire to hold the line. Here are a few thoughts that may help frame the discussion.

First, the concern is understandable. Wars are unsettling—both on a human level and for global economies and investment markets.

While history shows that stocks have typically been higher 6–12 months after the onset of a conflict, it’s one thing to see that in a table or chart and quite another to live through it. And yes, this time could be different.

Second, panic is a signal worth paying attention to. If a 5–10% decline is causing real stress, it may mean your current portfolio is too aggressive—at least for one household member. A portfolio only “works” if you can stick with it.

After all, pullbacks, corrections and bear markets are a regular feature of the stock market—see here and here. Your portfolio has to be built with both bull and bear markets in mind.

Third, there’s nothing wrong with dialing risk down to a “sleep-at-night” level. But, unlike your wife’s recommendation to move everything to cash and bonds, the choice doesn’t have to be all-or-nothing. Say your portfolio is currently around 75% stocks, and your spouse wants to go to 0% stocks. Is there a middle ground that both of you can live with?

Staying partially invested helps you participate in any recovery while reducing the emotional (and financial) strain of drawdowns.

Fourth, if you do move entirely to cash (or bonds), make a plan to get back in. This is critical—and often overlooked.

What would trigger a re-entry? A 20% market decline from your selling point? A 20% recovery? An end to the conflict (whatever that looks like)? No matter what you decide will be your triggers, write them down and review them regularly.

Without a plan, “temporary” moves have a way of becoming permanent—and that’s where long-term damage to wealth creation is done.

Finally, bring the conversation back to your goals. Are you still on track to meet them? And how would shifting to a more conservative portfolio change that outlook?

For example, if you’ve set aside several years’ worth of spending in cash, that cushion can give your portfolio time to recover without forcing you to sell at the wrong moment.

On the flip side, if moving to a conservative, lower-return portfolio (say, earning around 3% annually) still allows you to meet your goals, then you may not need as much stock exposure (and the anxiety that goes with it) as you currently have.

Generally, you should try to avoid making investment decisions when your emotions are running high. But we’re human—these reactions are natural.

The key is to find a portfolio that gives you (and your partner) the confidence to stay invested, even when it’s uncomfortable.

ETF Splits, Launches, Delays and Filings

Splits

Yesterday, Vanguard announced it will split the shares for five stock index ETFs on April 21, 2026:

- Growth ETF (VUG): 6-for-1 split

- MegaCap Growth ETF (MGK): 5-for-1 split

- S&P 500 Growth ETF (VOOG): 6-for-1 split

- MidCap ETF (VO): 4-for-1 split

- Information Technology ETF (VGT): 8-for-1 split

What does that mean if you own one of these ETFs?

In short, not much changes.

When an ETF splits, its price drops—but you receive more shares. The value of your investment stays the same.

Here’s a simple example.

Let’s say you own 100 shares of Information Technology ETF (VGT), which closed at $716.42 on March 23. Your position is worth $71,642.

After an 8-for-1 split, the share price would fall to about $89.55, and you’d own 800 shares instead of 100. Do the math, and your investment is still worth $71,642.

Different price. More shares. Same value.

So why bother with a split?

Vanguard says the goal is to “widen availability for investors by keeping share prices within accessible trading ranges.” Translation: Lower share prices make ETFs easier to trade.

That rationale makes sense for the growth and technology ETFs, which have surged in recent years and now sport some of the highest prices in Vanguard’s lineup.

But the decision isn’t entirely consistent. Why split MidCap ETF at around $290 per share, but leave S&P 500 ETF (VOO)—trading closer to $600—untouched?

Either way, if you own one of these ETFs, expect to see a sharp drop in price next month. It’s mechanical—not a reason for concern.

The bottom line: Vanguard has split ETF shares before and will likely do so again. But a stock split isn’t a reason to buy—or sell.

Launches

After hitting the pause button—twice—Vanguard appears ready to move forward. On Monday, the firm filed an updated prospectus with the SEC for its Target Maturity Corporate Bond ETFs.

There’s typically a short lag between a “final” filing and a fund’s launch, but all signs point to these ETFs becoming available before the end of the week.

Premium Members can read my full breakdown of these new ETFs here.

Delays

While the bond ETFs are nearly up and running, Vanguard has delayed the launch of Developed Markets ex-U.S. Growth Index ETF and Developed Markets ex-U.S. Value Index ETF. Originally scheduled for March 23, the ETFs are now expected to debut on April 10.

Premium Members can read my full take on these ETFs—and how they stack up against Vanguard’s legacy actively managed funds—here.

Filings

Last week, I told Premium Members that Vanguard had filed to launch its first junk-bond index ETF—the U.S. High-Yield Corporate Bond Index ETF (VCHY).

The ETF is due in June and fills an obvious hole in Vanguard’s lineup. Its competitors, iShares (HYG) and State Street (JNK), brought high-yield bond index ETFs to market nearly two decades ago.

One thing I got a bit wrong—or maybe “incomplete” is a better word—in my initial take was the potential for a fee war.

As I noted, the original high-yield bond ETFs (which are top of mind) charge 0.49% (HYG) and 0.40% (JNK). Given Vanguard’s actively managed High-Yield Active ETF (VGHY) costs just 0.22%, I expected its new index ETF to significantly undercut the competition.

But the landscape has already shifted.

It turns out that both iShares (USHY) and State Street (SPHY) already offer lower-cost alternatives charging 0.08% and 0.05%, respectively. In other words, the fee war has already happened in the junk bond ETF space—just not the way you might expect. Rather than cutting fees on the flagship funds, iShares and State Street launched cheaper versions (in 2017 and 2012, respectively) alongside them.

Apparently, the older ETFs are positioned as trading vehicles, while the newer ones are meant for long-term investors. How investors are supposed to distinguish between the two is another question entirely.

Three final thoughts.

First, it’s still reasonable to focus on HYG and JNK. Despite their higher fees, both funds continue to hold billions in assets. But investors do have lower-cost alternatives—and Vanguard is about to add another.

That persistence may explain why iShares and SPDR opted to launch new funds rather than cut fees on the originals.

I’ll let you decide what to make of that.

Second, while Vanguard’s lineup is getting more crowded, it’s still far less convoluted than its peers. At least Vanguard investors won’t have to choose between similarly named high-yield bond index ETFs with dramatically different expense ratios.

Third—the bottom line for Vanguard investors—we’re getting another high-yield bond arrow in our quiver. But it’s not one I’d reach for right now—we’re still not getting paid enough to take that risk.

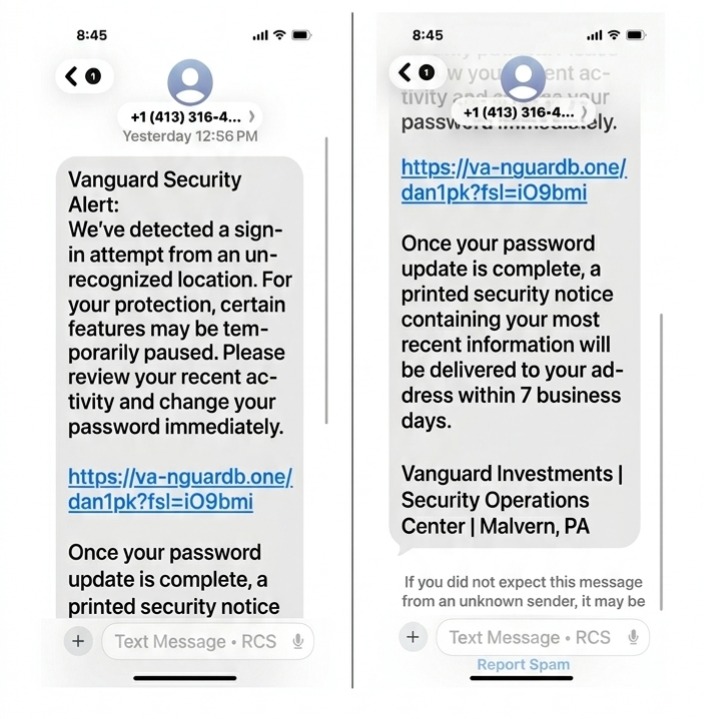

Scam Alert

Unfortunately, scammers are getting more sophisticated.

One IVA reader recently shared an experience that’s worth highlighting. As you can see in the screenshots below, he received a message that appeared to be from Vanguard—flagging an unrecognized login and urging him to change his password immediately.

Talk about nerve-wracking.

Fortunately, he did exactly the right thing: He ignored the message, picked up the phone and called a Vanguard number he knew he could trust. Vanguard confirmed it was a scam.

No harm done—just some time lost and a few frayed nerves.

The takeaway: If you receive a message that doesn’t feel right, do not click on any links. When in doubt, call a trusted number. (And don’t use the one provided in the suspicious message—look it up yourself.)

Lesson learned: A few minutes of caution can save you from a very costly mistake.

Our Portfolios

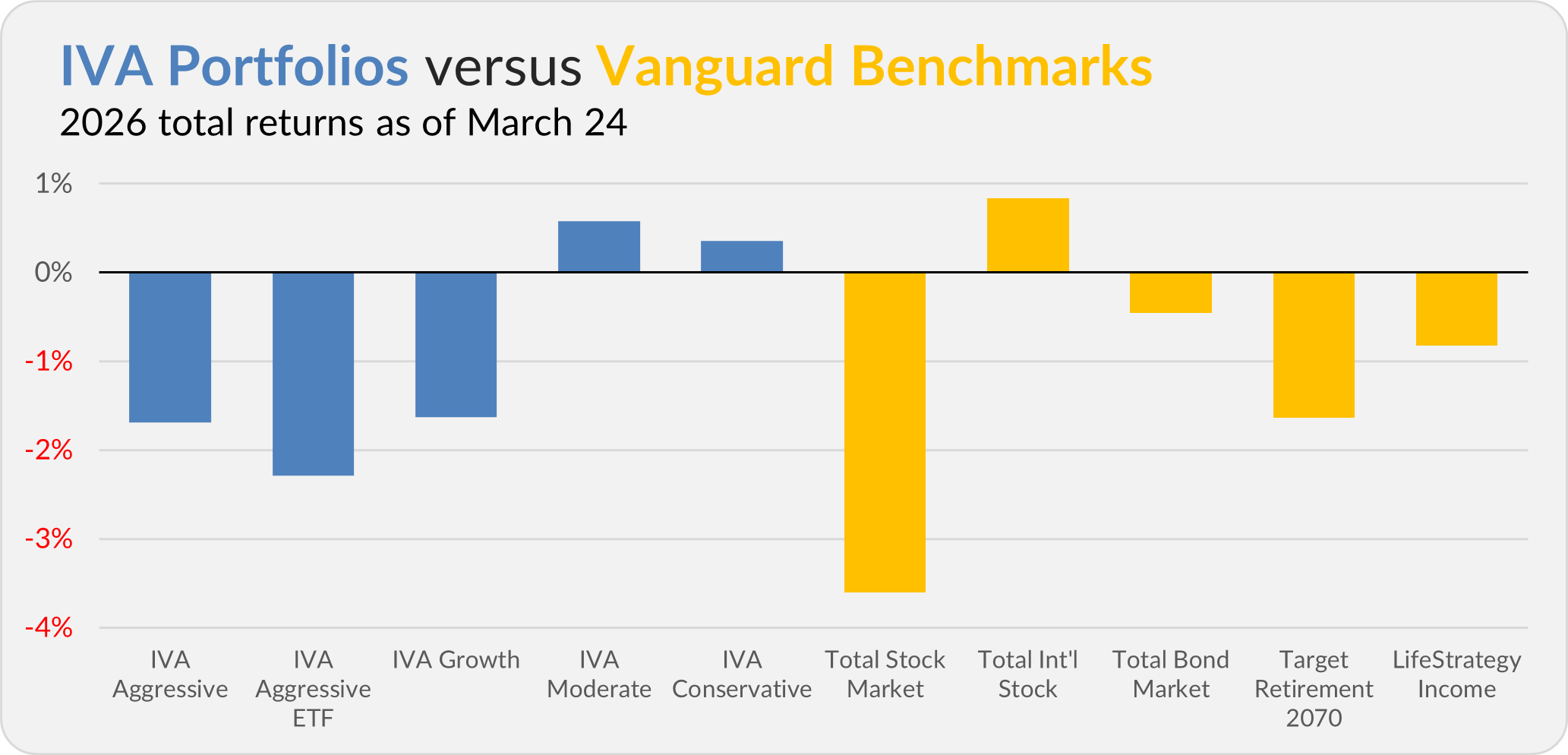

Our Portfolios are showing relatively decent returns for the year through Tuesday. The Aggressive Portfolio is down 1.7%, the Aggressive ETF Portfolio is off 2.3%, the Growth Portfolio is down 1.6%, the Moderate Portfolio is up 0.6% and the Conservative Portfolio is up 0.4%.

This compares to a 3.6% decline for Total Stock Market Index (VTSAX), a 0.8% gain for Total International Stock Index (VTIAX), and a 0.5% drop for Total Bond Market Index (VBTLX). Vanguard’s most aggressive multi-index fund, Target Retirement 2070 (VSNVX), is down 1.6% for the year, and its most conservative, LifeStrategy Income (VASIX), is down 0.8%.

IVA Research

Yesterday, I shared my exclusive conversation with MidCap Growth’s (VMGRX) new co-managers from Tremblant Capital—Brett Barakett and Michael Cling—with Premium Members.

Until my next IVA Weekly Brief, have a safe, sound and prosperous investment future.

Still waiting to become a Premium Member? Want to hear from us more often, go deeper into Vanguard, get our take on individual Vanguard funds, access our Portfolios and Trade Alerts, and more? Start a free 30-day trial now.

Vanguard and The Vanguard Group are service marks of The Vanguard Group, Inc. Tiny Jumbos, LLC is not affiliated in any way with The Vanguard Group and receives no compensation from The Vanguard Group, Inc.

While the information provided is sourced from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Additionally, the publication is not responsible for the future investment performance of any securities or strategies discussed. This newsletter is intended for general informational purposes only and does not constitute personalized investment advice for any subscriber or specific portfolio. Subscribers are encouraged to review the full disclaimer here.